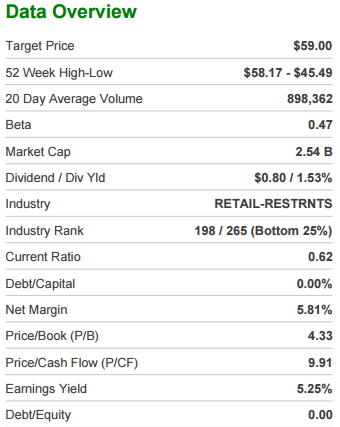

Summary:

Cheesecake Factory posted second-quarter 2016 results with earnings of $0.78

surpassing the Zacks Consensus Estimate by 11.4%. Also, earnings were up 13%

year over year on higher top-line and lower share count. Revenues of $558.9 million

missed the consensus mark by 0.6% but increased 5.7% year over year. Comps

increased 0.3% at Cheesecake Factory restaurants. Although comps were hurt by a

2.7% decline in traffic, it was partly offset by menu price increase of 2.9% and positive

mix of 0.2%. In fact, on the back of solid bottom-line performance in the second

quarter, the company increased its earnings guidance for full-year 2016. Meanwhile,

announcement of a 20% increase in the quarterly dividend should bolster investor

confidence in the company’s financials and therefore improve its market position.

However, higher costs and sluggish comps at the Grand Lux Café brand raises

concerns.

Reasons To Buy:

Strong Brand Recognition: Cheesecake Factory is one of the most recognized upscale

casual restaurants operating in the U.S. It taps all dining preferences from lunch and

dinner day parts to the mid-afternoon and late-night day part. Notably, the company

posted 26 consequent quarters of positive comps at The Cheesecake Factory

restaurants. Cheesecake Factory is well positioned to sustain its same-stores sales

growth owing to a constant increase in guest traffic.

Focus on Expansion: Despite challenging economic conditions, Cheesecake Factory has been expanding in the domestic as well as

international markets. The restaurants opened over the past three years are performing better than the erstwhile locations. The

company remains focused on opening its restaurants at high grade sites to hit targeted returns. Besides the domestic market, the

company is of late foraying into lucrative markets like the Middle East, North Africa, Central and Eastern Europe, Russia, Turkey,

Mexico, Kuwait and Lebanon and Chile. In 2016, the company plans to open eight company-owned restaurants along with four to

five restaurants internationally under licensing agreements.

Also, the company recently launched a Cheesecake Factory outlet at the Shanghai Disney Resort– marking the company’s entry in

China, East Asia, a region known for its economic growth and healthy investment returns. The region boasts a relatively younger

population and a growing middle class with higher disposable income. Therefore, entry into this market will further boost traffic and

comps.

Initiatives to Boost Sales: The company is committed to boost its sales and improve margins to survive in the competitive

environment. In order to boost comps, the company is focusing on improving its speed of service and training its servers so that they

render higher level of service.

Meanwhile, given consumers preference for healthy food, the company introduced a new category called Super Foods last year. It

features items that contain nutrient rich ingredients such as kale, blueberries, almonds, salmon and quinoa. Going forward, the

company intends to carry on with menu innovation by adding new Super Food items as well as the famous The Cheesecake Factory

indulgences.

Moreover, in the second quarter of 2016, the company completed the rollout of its new server training program. Also, in order to

capitalize on the latest technology, the company rolled out its mobile payment app, CakePay. Cheesecake factory has also

increased its focus on home and office delivery and is currently piloting a delivery service with a third-party partner in select

locations.

Additionally, the company continues to focus on its gift card program. Gift card sales increased approximately 25% on an average in

each of the past two years. These initiatives would help the company to continue to keep up the trend of positive comps.

Focus on Improving Margins: The company is evaluating different approaches to limit its costs. It installed a cost management

system with substantial capabilities across production, planning and inventory management a few years ago to help analyze usage

and waste. Amid current soft environment, such efforts to control costs would help to improve margins.

Cash Deployment Strategy: Cheesecake Factory continuously returns wealth to shareholders via dividends and share repurchases.

The company returned $141 million in cash via share buybacks and dividends in 2015, higher than its target.

Moreover, the company has continuously paid quarterly dividends since it announced its first dividend payment of $0.12 per share in

2012. Since then, the company has increased its dividend four times, by 17%, 18%, 21% and 20% in 2013, 2014, 2015 and 2016,

respectively.

Risks:

Rising Costs to Keep Profits Under Pressure: Of late, the company’s profits have been under pressure owing to a rising wage

rates scenario. Moreover, the company’s unit expansion plans, pre-opening costs of outlets and costs related to sales initiatives

are major headwinds.

Soft Consumer Spending: The restaurant industry has been experiencing low consumption over the last few quarters. Despite

moderate improvement in economic growth, consumers are increasing their spending only modestly as an increase in jobs this

year is yet to translate into significantly higher wages. Higher health care costs and still-tightened credit availability continue to

hurt consumer discretionary spending in the U.S. As a result, Americans are unwilling to dine out, which is pulling down the

company’s sales.

Continued Sluggish Performance in Grand Lux Cafe: Continued underperformance of Grand Lux Cafe remains a matter of

concern. Segment comps have been declining over the past few quarters as the company has been increasing menu prices.

These menu price increases amid a soft consumer spending environment have been hurting traffic trends and thereby comps. In

fact, owing to higher wage rate, the company intends to once again increase menu prices in the near term. This would further hurt

traffic.